It happens that situations arise when, when entering all the documents, the expected expenses are not displayed in the book of expenses and income.

Let's look at the most common reasons why expenses reflected in accounting are not displayed in KUDIR.

1. Props “Expenses (OU)”

In accordance with Art. 346.16 of the Tax Code of the Russian Federation, the list of accepted expenses is closed, i.e. Only those expenses that are explicitly listed in this article can be taken into account as expenses.

When reflecting expenses in the program, it is indicated whether these expenses are accepted or not, that is, they comply with the requirements of Art. 346.16 of the Tax Code of the Russian Federation or not.

For example, in the document “Receipt of goods and services”, reflecting the services of a third-party organization, it will look like this.

Fig. 1 “Document - Receipt of goods and services”

It is worth noting that expenses are considered not accepted if the “Expenses (OU)” detail is not filled out.

When it comes to goods and materials, there are certain difficulties. For them, the acceptability of expenses is determined by both receipt and write-off.

For example, despite the fact that in the receipt document it is indicated “accepted” for materials and goods, expenses for them will not be accepted if, for example, the materials were written off as non-acceptable expenses, and the goods were sold as part of activities subject to UTII.

Another example is the free supply of materials. Such materials will not be accepted as expenses. Even if the requirement - invoice indicates “accepted”, in the receipt document in the column “Expenses (OU)” it will be indicated “not accepted”.

2. Payment and other necessary conditions

As required by the cash method, expenses will be recognized only after actual payment has been made.

For certain types of expenses there are additional conditions, for example, expenses for the purchase of goods cannot be accepted before they are sold.

The program automatically monitors all necessary conditions, and until all necessary events are reflected, the consumption will not be displayed in KUDIR. Therefore, the second reason may be the fact that the expenses were not paid or certain events that are necessary to recognize the expense did not occur.

3. Sequence of documents

One of the most common reasons is backdating of documents.

When working with documents backdated, it is necessary to repost all later documents associated with these expenses. If you cannot establish a connection, you will have to rewire everything.

4. Opening balances

In the simplified taxation system, special accounting is kept in special accrual registers. These registers contain information about consignments of goods and materials, mutual settlements, and specific information about expenses.

Initial balances must be entered into these registers, that is, if there are expenses that are associated with operations incurred before the start of accounting or before the transition to a simplified taxation system, then this information must be entered. If you do not enter initial balances, then expenses may not be included in KUDIR, here is another reason.

5. Accounting validity date

In “1C: Accounting 8” there is a mechanism that allows you to split the document posting into two stages to speed up the work - quick registration of the document and final posting in batch mode. In this mechanism, there is such a thing as the date of relevance of the accounting - before this date, the accounting is current and the documents have been completed in full, and after this date the documents still await final completion. In view of this, expenses may not be recognized if the document is not fully posted (located after the date of relevance).

6. Mutual settlements using settlement documents for tax accounting only

This situation is quite rare, but since it is difficult to identify on your own, it deserves a separate description.

In 1C: Accounting 8, accounting for mutual settlements under an agreement with a counterparty can be maintained in two ways:

- According to the agreement as a whole;

- According to settlement documents.

Accounting for mutual settlements for the purposes of the simplified tax system works the same way. It is possible that in the accounting settings the maintenance of the “Settlement document with the counterparty” analytics is disabled, but agreements “based on settlement documents” are used. In this case, according to accounting, it is not noticeable that advances and payments are not closed, and in tax accounting, expenses are considered unpaid and are not reflected in KUDIR.

In such a situation, it is recommended to correctly fill in the “settlement document” details in the documents or refuse to use agreements with mutual settlements “according to

settlement documents" and use instead an agreement with mutual settlements under the "agreement as a whole".

Analysis of the state of expenses subject to reflection in tax accounting according to the simplified tax system

The accumulation register “Expenses under the simplified tax system” stores information about each expense of the organization, which can be reflected in the KUDIR.

The information of greatest interest is:

- for what reasons and what expenses are not accepted for tax accounting;

- What needs to be done to ensure that these expenses are accepted for tax accounting.

Expense statuses can take the following values:

- Not written off;

- Not written off, not paid;

- Not paid;

- Not paid, not paid by the buyer;

- Not paid by buyer.

In the report, set the following settings (Figure 2-3).

All taxpayers using the simplified taxation system (STS) are required to keep a book of income and expenses (KUDiR). If you do not do this, or fill it out incorrectly, you can receive a considerable fine (Article 120 of the Tax Code of the Russian Federation). This book is printed and submitted to the tax office upon their request. It must be sewn and numbered.

Before you start creating this income and expense accounting book in 1C 8.3, check the program settings. If you have problems with the formation of KUDiR and some expenses do not fall into the book, carefully double-check the settings. Most of the problems lie here.

Where is the income and expense accounting book 1C 8.3? In the "Main" menu, select the "Settings" section.

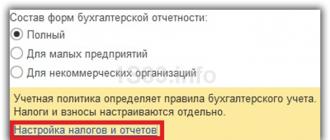

You will see a list of configured accounting policies by organization. Open the position you need.

In the accounting policy setup form, at the very bottom, click on the “Set up taxes and reports” hyperlink.

In our example, the “Simplified (income minus expenses)” tax system was selected.

Now you can go to the “STS” section of this setting and configure the procedure for recognizing income. This is where it is indicated which transactions reduce the tax base. If you have a question why an expense does not fall into the book of expenses and income in 1C, first of all look at these settings.

Some items cannot be unchecked as they are required to be filled out. The remaining flags can be set based on the specifics of your organization.

After setting up the accounting policy, let's move on to setting up the printing of the KUDiR itself. To do this, in the “Reports” menu, select the “STS Book of Income and Expenses” section of the “STS” section.

The ledger report form will open in front of you. Click on the "Show Settings" button.

If you need to detail the records of the received report, check the appropriate box. It is better to clarify the remaining settings with your tax office, having learned the requirements for the appearance of KUDiR. These requirements may vary between inspections.

Filling out KUDiR in 1C: Accounting 3.0

In addition to the correct settings, before generating KUDiR, it is necessary to complete all operations for closing the month and check the correctness of the sequence of documents. All expenses are included in this report after they are paid.

The D&R accounting book is generated automatically and quarterly. To do this, you need to click on the “Generate” button in the form where we just made the settings.

The book of income and expenses contains 4 sections:

- Section I. This section reflects all income and expenses for the reporting period quarterly, taking into account the chronological sequence.

- ChapterII. This section is filled out only if the simplified tax system is “Income minus expenses”. This contains all costs for fixed assets and intangible assets.

- ChapterIII. This contains losses that reduce the tax base.

- ChapterIV. This section displays amounts that reduce tax, for example, insurance premiums for employees, etc.

If you have configured everything correctly, then KUDiR will be formed correctly.

Manual adjustment

If, after all, KUDiR is not filled out exactly as you wanted, its entries can be corrected manually. To do this, in the “Operations” menu, select “STS Income and Expense Book Entries.”

In the list form that opens, create a new document. In the header of the new document, fill in the organization (if there are several of them in the program).

This document has three tabs. The first tab corrects the entries in section I. The second and third tabs are in section II.

If necessary, make the necessary entries in this document. After this, KUDiR will be formed taking into account these data.

Analysis of accounting status

This report can help you visually check whether the book of income and expenses is filled out correctly. To open it, select “Accounting analysis according to the simplified tax system” in the “Reports” menu.

If the program keeps records for several organizations, you need to select in the report header the one for which the report is needed. Also set the period and click on the “Generate” button.

The report is divided into blocks. You can click on each of them and get a breakdown of the amount.

All individual entrepreneurs (IP) and organizations using the simplified tax system must submit an income tax return to the tax office. To determine the amount of profit, it is necessary to maintain a register of financial transactions during their activity.

For this purpose it is used book of income and expenses. How to properly register transactions to avoid penalties?

Definition, decoding and composition

The abbreviation KUDiR is created from the first letters of the phrase “book of income and expenses.”

During the implementation of activities, financial transactions determined by the Tax Code of the Russian Federation are registered in it, confirmed by such documents:

During the implementation of activities, financial transactions determined by the Tax Code of the Russian Federation are registered in it, confirmed by such documents:

- bank statements;

- and warrants;

- invoices (for example,);

All types expenditure actions, subject to registration in the book, are indicated in two articles of the Tax Code of the Russian Federation - 249 and 250. There are also some types of costs, which are also subject to registration on the basis of the first paragraph of Art. 346.16 Tax Code. The entry on the payment of the minimum tax is not entered, because this does not equate to expense items.

Fixing the amount expense transactions are carried out only after receipt of the goods or services and full payment of their cost. For example, a periodic monthly payment for renting a premises can be made no earlier than the last day of the month for which the amount is transferred to the landlord.

Confirming there will be a payment order from the bank; and the deed of transfer in connection with the rental of the premises.

Income receipts are recorded on the pages of the book using the cash method. Advance transactions are also registered on the day of receipt of the advance payment, entering data from the confirming primary document.

If during an inspection an individual entrepreneur or an organization with a simplified tax system does not have a KUDiR, then they are subject to a fine. Its size is 10 thousand rubles for organizations, and 200 rubles for individual entrepreneurs.

Rules for maintaining a book

Individual entrepreneurs, organizations with the simplified tax system and those using . There is no need to register it with the tax office, because this rule has been abolished since 2013. Based on the brochure account data, taxes are calculated and a declaration is prepared for the tax office.

Management options There are only two of this book:

Management options There are only two of this book:

- The handwritten method is used to fill out special forms, numbered into a single document.

- An electronic method of maintaining a record of financial transactions, which is maintained throughout the calendar year in a digital code. Then at the end of the year the pages are printed, numbered and stapled.

At the beginning of each calendar year, a new accounting book for income and expenses is created. Information on paper about the taxpayer's annual activities must be stored for 4 years.

Attention! The presence of a book is not canceled for taxpayers who do not carry out economic activities during the reporting periods.

How to correctly fill out the Income and Expense Accounting Book is discussed in the following video:

If you have not yet registered an organization, then easiest way This can be done using online services that will help you generate all the necessary documents for free: If you already have an organization and you are thinking about how to simplify and automate accounting and reporting, then the following online services will come to the rescue and will completely replace an accountant at your enterprise and will save a lot of money and time. All reporting is generated automatically, signed electronically and sent automatically online. It is ideal for individual entrepreneurs or LLCs on the simplified tax system, UTII, PSN, TS, OSNO.

Everything happens in a few clicks, without queues and stress. Try it and you will be surprised how easy it has become!

Registration

Maintaining KUDiR differs depending on the chosen one, so you need to choose a special form for such tax reporting systems:

Title page and pages number and with the help of a cord they are combined into a brochure. On the last sheet the knot is sealed. The pasted piece of paper indicates the number of pages in the document, certified by a signature and seal, if any.

Errors may be made when entering data on payment transactions, but there is a possibility of them to correct. In principle, there is nothing terrible here, because... erroneous data can be easily corrected in the following ways:

- in the electronic record by removing incorrect parameters and replacing them with correct information.

- When filling it out in handwriting, you must cross out the indicator and enter accurate information. Each correction is confirmed by the signature of the manager with a seal ().

What punishment threatens the taxpayer? for unreliable information in KUDiR? If the tax was calculated incorrectly based on incorrect parameters, you will have to pay 20% of its amount in the form of a fine. Deliberate concealment of information about parameters, due to which the amount of tax liabilities paid was reduced, is punishable by a penalty of 40% of the tax.

It is possible to prevent the application of sanctions for unreliable accounting in KUDiR if tax payments are paid on time. But they must be calculated correctly, even if the data taken from the brochure is incorrect. For payment of tax in full under such circumstances, the penalty is subject to cancellation.

Fill Tabular data on income and expenses need to be very careful. The tax service is always interested in the justification of cost items and supporting primary documents. Replenishment of an individual entrepreneur's bank account from personal funds is not reflected in the income for this book. The same applies to increasing the organization due to the receipt of an interest-free loan.

Explanations about the content of KUDiR are discussed in this video material:

Filling procedure

The book begins with title page, which reflects:

- details of the individual entrepreneur or organization;

- start date of entering accounting transactions;

- object of taxation, where the phrase either “income” or “Income plus expenses” is indicated.

First section contains information about quarterly income and expenses. It contains four tables - for each quarter of the year. The fields in them are divided into 5 columns:

- No.;

- date and number of the financial document confirming the expenditure or receipt transaction;

- content of the operation;

- the amount of income to be included in the tax base;

- expenses that need to be taken into account when calculating the tax base.

The section ends with a certificate, which organizations with “income” do not fill out.

Second section subject to entering data on expenses for the acquisition of fixed assets and intangible assets. Only organizations using the simplified tax system “Income minus expenses” fill out this section. Fixed assets include real estate and equipment used in business for more than 12 months. Intangible assets include intellectual developments, rights to inventions, etc.

Second section subject to entering data on expenses for the acquisition of fixed assets and intangible assets. Only organizations using the simplified tax system “Income minus expenses” fill out this section. Fixed assets include real estate and equipment used in business for more than 12 months. Intangible assets include intellectual developments, rights to inventions, etc.

Third section also filled out only by organizations using the simplified tax system “Income minus expenses.” In the fields of the section, parameters of losses related to the previous tax period or current ones, which can be reflected in the future, are entered.

Fourth section is allocated for filling out by taxpayers on the simplified tax system “Income”. The main indicators that need to be entered here are paid. These parameters reflect “for yourself” and hired workers.

Nuances of using KUDiR

Registration of financial transactions in KUDiR during business activities is different for each type of simplified taxation.

But for all taxpayers the following is established: general procedure for entering information:

But for all taxpayers the following is established: general procedure for entering information:

- records are made in Russian;

- the book records only transactions during the tax period when carrying out activities that are involved in the calculation of tax liabilities;

- each entry is made according to data from the primary document;

- The chronology of records for each individual operation is maintained.

In tables, you cannot arrange records by day or type of transaction. Each specific operation must be entered on a separate line.

What other nuances exist when filling out tabular data can be understood by looking at examples of recording income and expense transactions.

With simplified tax system

For the first section, information is entered into quarterly tables line by line. Here we can recommend that in column two you reflect not only the number and date of the operation, but also the name of the primary document.

If no activity was carried out during the tax period, you need to fill in the zero KUDiR. It fills in the data on the title page, and leaves all other pages blank.

If no activity was carried out during the tax period, you need to fill in the zero KUDiR. It fills in the data on the title page, and leaves all other pages blank.

For simplifiers under the simplified tax system "income" 6% It is necessary to enter income into the columns of the 4th column. For example, money was received for a service provided in the amount of 5 thousand rubles. according to check No. 2 dated February 15, 2016. In this case, the cost of the service is 5 thousand rubles. entered in column 4. An overpaid amount for the service was identified in the amount of 500 rubles, which was returned to the client on May 16, 2016. The serial number, check and date of the refund are recorded in a separate line, and the amount is entered in the 4th column with a minus sign “-500”.

Only Income is filled out on the simplified tax system (USN) 6%. Please note that this section should not include all insurance premiums, but only those that reduce the simplified tax.

Transactions in the book are recorded using the cash method, i.e. on the day of receipt or payment of funds.

If used Simplified tax system “income minus expenses”, then the readings are entered into the income columns, as in the previous simplified tax system, “income” of 6%. At the same time, pay more attention to filling out the expense columns.

For example, they make the following cost information separately for each event:

- Goods for resale - the primary document is the issued Consignment Note No. 1092 dated February 26, 2015.

- Services, write the date of expenditure for the service and the report number. For example, 04/30/2015 Check No. 00000003.

- Expenses are paid in cash, which we enter from the sales receipt: date and number. Example: 05/25/2015 Check No. 00000014.

- Return: you sold some product (provided a service), and you were paid more. Then you refunded the overpaid amount to the client. In this case, you need to reduce the “Income” column, for which you reflect (according to the actual date of the surplus given) in it, in the same way as in the previous version, a negative amount.

Expenses for the purchase of goods are fixed after receiving funds from its sale.

Patent

If the activity is carried out on a patent (PSN), then you need to use the KUDiR form, approved for use since 2013. Only income columns are filled in the lines, because When using a patent, expenses are not subject to registration in KUDiR.

BASIC

Organizations on OSNO KUDiR is not used. IP on OSNO keep a special book with. It differs significantly from that used under the simplified tax system, because information is provided on pages that differ significantly.

The rules for designing a Book in electronic form using 1C are outlined in the following video lesson:

Changes for 2019

Starting from 2018, the Book of Income and Expenses contains an additional fifth section. It must be filled out by those who pay tax to the simplified tax system on income of 6%. This section indicates the amount of the trading fee. This allows this category of taxpayers to reduce the amount of contributions paid to the budget by the amount of the trade tax. The remaining rules for filling out KUDiR remained unchanged.

Colleagues!

Often in our practice, questions arise regarding the acceptance of expenses in KUDiR.

It seems like they did everything: they received and entered the invoice into the database, paid the invoice to the supplier, shipped the goods to the buyer, but the expenses are not recorded in KUDiR.

So what should I do?

You have to enter these expenses using the Entry document in the Book of Income and Expenses.

But this means doing double work and possibly getting an error in the future.

So, let's try to answer the question “why” this happens and how to check whether the conditions for accepting expenses as expenses are met.

So let's begin...

Preliminary notes: we consider the accounting policy settings:

- Accounting policy - tab of the simplified tax system - Procedure for recognition as expenses:

It all depends on the accounting policy settings.

We carefully analyze the noted data: in order of recognition of expenses it is worth

Receipt of goods, payment for goods and sale of goods. Those. If you have the “Sale of goods” checkbox, then paying for the goods and posting the goods to recognize expenses in KUDiR will not be enough for you. Then the costs will be included in KUDiR expenses only after the goods have been shipped. And if the “Receiving income (payment from the buyer)” checkbox is checked, then receiving payment from the buyer.

This is the most important thing to always start checking with.

2. The second very important point: checking the accounting of expenses in NU.

This will have to be done by checking vocational school documents, invoice requirements, etc., where there is an accounting of NU Expenses. The cost item may have been selected incorrectly ( not taken into account expenses at NU).

3. If everything is according to paragraphs. 1-2 You have checked, then work begins with the accumulation register of Expenses under the simplified tax system.

Build a report on it in the Universal Report with a selection for the expense element that is not taken into account in KUDiR and analyze the data obtained.

Using the data in the “Expenses under the simplified tax system” register, you can determine which expenses have not yet been accepted for tax accounting, for what reasons, and what must happen for a specific expense to be accepted for tax accounting.

General scheme for accepting expenses:

— Receipt of goods (PTU): Not written off, not paid

— Payment to the supplier (Statement): Not written off

— Sales (RTU): Not paid by the buyer

— Payment from the buyer (Statement): Accepted as expenses.

Depending on what you have in your accounting policy, the last two conditions may or may not be taken into account when accepted as an expense.

In our case, the “Unpaid” status shows that you have not paid for vocational training to the supplier, therefore you cannot accept the amounts as expenses

And the Status is “not written off” - there is no sale of the purchased goods, so again it cannot be accepted as an expense.

Status “not written off, not paid” - the product has not been paid to the supplier and there is no sale for it.

Here is an example of compiling a report on the accumulation register of Expenses under the simplified tax system: